You finally decide to join a medical scheme. You submit the forms, you feel organised, and then you see the contribution is higher than you expected. Someone mentions a late joiner penalty (otherwise referred to as an LJP) and suddenly it feels like you missed something important.

Take a breath. This is one of those topics that sounds intimidating until it’s explained plainly. Here’s what a late joiner penalty is, when it can apply, how it’s calculated, and what to check before you join. (And if you want a second set of eyes, we will show you when it makes sense to speak to MedXpert.)

What is a Late Joiner Penalty

The plain language definition

A Late Joiner Penalty is an extra percentage added to your monthly medical scheme contribution when you join a medical scheme after the age of 35 and have not belonged to a medical scheme for a period before that. The rules sit in the Medical Schemes regulations (Regulation 13) and are used across schemes.

In everyday terms: if you only join a scheme at a point where you are statistically more likely to claim, and you have not been a scheme member for long enough before then, the scheme may charge more for the risk they are taking on.

Why medical schemes use it

Medical schemes work by pooling risk. When people join only once they are older (and on average more likely to need medical care), it can put pressure on the pool. A late joiner penalty is a policy tool that aims to protect the sustainability of the scheme by adjusting contributions for late joiners who did not contribute to the pool earlier.

This is not about “punishing” you. It is a rule-based way schemes manage long-term risk, ensuring that the pool of funds used to pay for everyone’s claims doesn’t run dry.

When can a scheme apply a Late Joiner Penalty

The age milestone and the “late” rule

A scheme may apply a late joiner penalty to a member (or adult dependant) who is 35 years or older and meets the definition of a late joiner in the regulations. The rules focus on your membership history. You might have either not been on a medical aid at all before now, or you only have a limited amount of time spent as a medical scheme member.

What counts as creditable coverage prior medical scheme membership

“Creditable” membership refers to the time you spent as a dependent or principal member of a registered South African medical scheme prior to your new application. This history of membership must be proven with legal documentation, such as previous membership certificates showing the start and end date or, in certain cases, a signed affidavit.

One important detail: periods where you were a dependant under 21 are typically excluded from the creditable years’ calculation.

If you are unsure what in your history will count, do not guess. Confirm it with MedXpert.

Breaks in membership and the 3-month rule

Even if you were on a scheme before, a break in membership longer than three consecutive months can matter. Where the rules treat the break as significant, your “creditable years” may not protect you in the way you assumed. This is because, once those three months have passed, all underwriting becomes applicable again.

How the Late Joiner Penalty is calculated

The official LJP formula, explained simply

The regulations use a formula to work out your uncovered years after age 35:

A = B − (35 + C)

A = years without medical aid cover (used to find your penalty band)

B = your age when joining a registered medical scheme

C = your years of creditable membership and coverage

If A is 0 or negative, you generally do not fall into a penalty band (because you have no uncovered years after 35, based on what the scheme recognises as creditable).

Important: Medical insurance membership history will be excluded from the calculation, as well as cover provided by a product from another country. Creditable cover is specific to cover with a registered South African medical aid scheme.

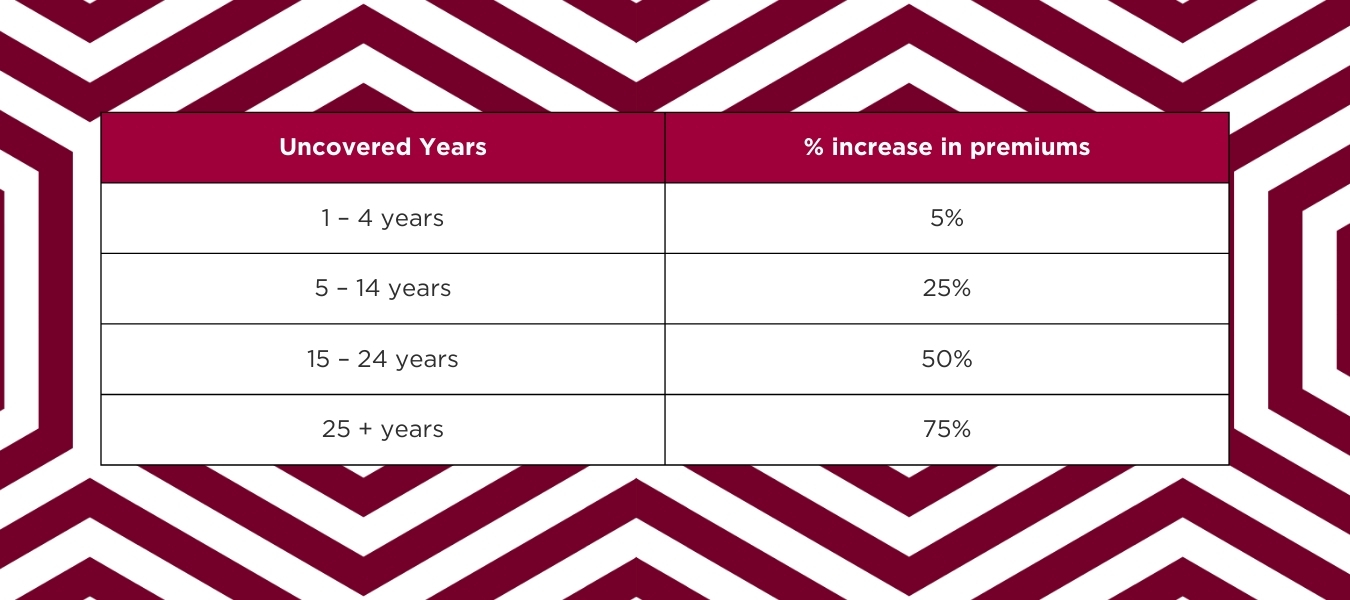

The Late Joiner Penalty bands and what they mean

Once your uncovered years are calculated, the maximum penalty bands are:

These are maximum bands. A scheme may apply a lower penalty, but it cannot exceed these bands.

Let’s use a realistic example.

Scenario: You are 58 and you can prove 12 years of creditable medical scheme membership. (Remember, dependant membership under 21 usually doesn’t count.)

- Start with the formula: A = B − (35 + C)

- Insert the details: A = 58 − (35 + 12)

- Calculate the brackets first: 35 + 12 = 47

- Subtract your age with the answer from the brackets: 58 − 47 = 11

11 uncovered years falls into the 5–14 band which is a 25% late joiner penalty.

Important: the scheme confirms the final outcome based on the proof of membership you provide.

What the penalty gets added to

Risk portion vs savings portion

Many people look at the total contribution and feel blindsided. It helps to know that late joiner penalties are generally applied to the part of the contribution linked to insured risk benefits. In practice, this is usually the risk portion, not the medical savings portion. The late joiner penalty also only applies to the membership costs of the specific person that the penalty applies to, so if you have four people on your plan but only one person has an LJP then the penalty is only applied to the cost of that single person.

Risk portion: the part that funds insured benefits like hospital and day-to-day insured benefits (depending on the option).

Savings portion: your personal savings account component (if your option has one). If your plan includes savings, ask the scheme to confirm whether the penalty applies only to the risk portion and to provide a clear breakdown of the contribution.

How long the penalty lasts

What “permanent” usually means in practice

A late joiner penalty is not a once off fee. It stays in place for as long as you remain on that medical scheme, because it is a pricing adjustment tied to your membership history at the point of joining the scheme.

There is also a practical nuance many people miss: if a penalty has already been imposed and you later provide additional proof of creditable membership, the scheme must recalculate the penalty and apply the revised penalty from the time you provided the evidence.

So, if your paperwork improves, your position may improve too, but you need to supply the evidence.

Contact MedXpert for expert help today.

Late Joiner Penalty vs waiting periods

Why people confuse them

They often come up in the same conversation when you are joining. Both can affect your experience as a new member, but they do it in very different ways, and confusing them can lead to frustration.

The key difference in one clear comparison

Late joiner penalty: affects what you pay every month. Waiting periods: affect when certain claims can be paid, typically for a limited time after joining, and are linked to underwriting rules rather than “late joining” itself.

What to check before you apply

Your personal checklist

Use this as a calm, practical checklist before you submit an application:

- Confirm your age at application (the 35+ milestone matters).

- List every period (even if it was only for a few months) you were on a registered South African medical scheme, whether you where the principal member or a dependant.

- Note any breaks in membership, especially anything longer than three consecutive months.

- Estimate your uncovered years using the formula (so you can budget).

- Ask MedXpert to confirm whether a penalty will apply and, if so, which band.

- Collect the documents that help you prove prior membership.

Proof is where most people get stuck. Start gathering:

- Membership certificates or membership history letters from previous schemes.

- Any documentation showing start and end dates of membership.

- Evidence for periods where you were a dependant (noting that under-21 periods usually do not count for the calculation).

- Membership numbers linked to prior membership.

If you cannot obtain proof after reasonable effort, ask the scheme what alternative evidence they accept and whether a sworn affidavit is an option in their process.

According to Regulation, a sworn affidavit will be accepted if the following conditions are met:

- The relevant periods in which you were a member or dependant and the name(s) of the relevant medical schemes corresponding with such period(s); and

- That reasonable efforts have been made to obtain documentary evidence of such periods of creditable coverage but have been unsuccessful.

A practical tip: request these documents early. Admin can take time, and you do not want your application delayed simply because paperwork is missing.

Questions to ask the scheme before you join

Ask directly and keep it simple:

- “Based on my membership history, will a late joiner penalty apply?”

- “If yes, what is the percentage that will apply to my contributions?”

- “Is the penalty applied to the risk portion only, and can you share the contribution breakdown?”

- “What proof of prior membership do you require, and what happens if I submit more proof later?”

If you would like help preparing these questions and organising your membership history, MedXpert can guide you through the process so you know what you are walking into before you commit.

When to speak to MedXpert

Situations where guidance saves time and stress

It is worth speaking to MedXpert when:

- You are 35 or older and are unsure how your history will be counted.

- You have had breaks in membership and cannot tell if they exceed three months.

- You were a dependant for long periods and do not know what will count as creditable.

- You cannot find proof of membership and need to understand practical options for replacing missing information.

- You want to compare options fairly, with the penalty (if any) reflected in your real monthly budget.

What MedXpert can help you confirm and compare

MedXpert can help you:

- Interpret your membership history against scheme rules in plain language.

- Identify what documents you need and how to request them.

- Sense-check an estimated penalty band before you apply.

- Compare options realistically, so you understand the likely contribution impact and what you are paying for.

Speak to MedXpert to help you confirm whether a late joiner penalty may apply and to compare options clearly, based on your situation.

FAQ

Can I avoid a Late Joiner Penalty?

If you have sufficient creditable membership (as recognised by the scheme) and no disqualifying breaks, you may not fall into a penalty band. The best way to avoid surprises is to confirm your membership history and ask the scheme to confirm your position before joining.

Does the penalty fall away?

In practice, the LJP is treated as ongoing for as long as you remain on the scheme. If you later provide additional evidence of creditable membership, ask the scheme to recalculate the penalty from the date you supplied the proof.

Note: It’s not uncommon that a membership will be terminated because the member considers the LJP an issue, which is understandable. It is, however, very important to remember that your time without medical aid coverage will only grow if you choose to cancel your medical aid. In other words, if you only have 4 years wherein you were not covered by a medical aid then you will have a 5% penalty, but if you choose to cancel and go another year without cover then your total years will increase to 5 years, which pushes you into the next LJP bracket, so if you join another scheme then your LJP will be 25%.